题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[单选题]

Goods are carried by several () of transport--on road or rail, by sea or air.

A.means

B.roads

C.ships

答案

答案

查看答案

请输入或粘贴题目内容

搜题

请输入或粘贴题目内容

搜题

拍照、语音搜题,请扫码下载APP

题目内容

(请给出正确答案)

拍照、语音搜题,请扫码下载APP

题目内容

(请给出正确答案)

A.means

B.roads

C.ships

答案

更多“Goods are carried by several () of transport--on road or rail, by sea or air.”相关的问题

更多“Goods are carried by several () of transport--on road or rail, by sea or air.”相关的问题

第1题

A、roads

B、means

C、ships

第2题

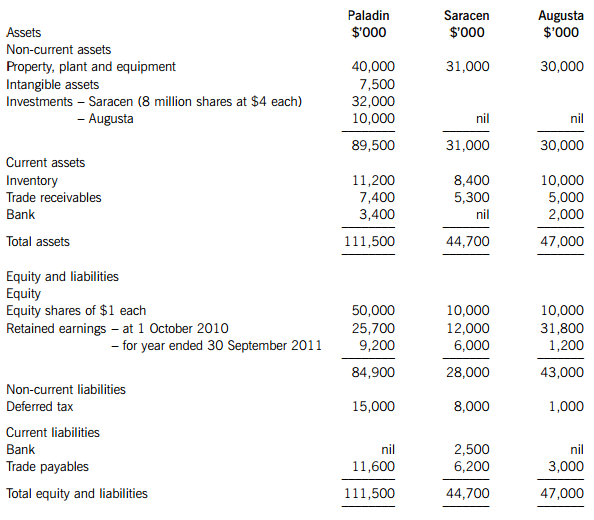

an immediate payment of $4 per share on 1 October 2010; and

a further amount deferred until 1 October 2011 of $5·4 million.

The immediate payment has been recorded in Paladin’s financial statements, but the deferred payment has not been recorded. Paladin’s cost of capital is 8% per annum.

On 1 February 2011, Paladin also acquired 25% of the equity shares of Augusta paying $10 million in cash. The summarised statements of financial position of the three companies at 30 September 2011 are:

The following information is relevant:

(i) Paladin’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose the directors of Paladin considered a share price for Saracen of $3·50 per share to be appropriate.

(ii) At the date of acquisition, the fair values of Saracen’s property, plant and equipment was equal to its carrying amount with the exception of Saracen’s plant which had a fair value of $4 million above its carrying amount. At that date the plant had a remaining life of four years. Saracen uses straight-line depreciation for plant assuming a nil residual value. Also at the date of acquisition, Paladin valued Saracen’s customer relationships as a customer base intangible asset at fair value of $3 million. Saracen has not accounted for this asset. Trading relationships with Saracen’s customers last on average for six years.

(iii) At 30 September 2011, Saracen’s inventory included goods bought from Paladin (at cost to Saracen) of $2·6 million. Paladin had marked up these goods by 30% on cost. Paladin’s agreed current account balance owed by Saracen at 30 September 2011 was $1·3 million.

(iv) Impairment tests were carried out on 30 September 2011 which concluded that consolidated goodwill was not impaired, but, due to disappointing earnings, the value of the investment in Augusta was impaired by $2·5 million.

(v) Assume all profits accrue evenly through the year.

Required:

Prepare the consolidated statement of financial position for Paladin as at 30 September 2011.

第3题

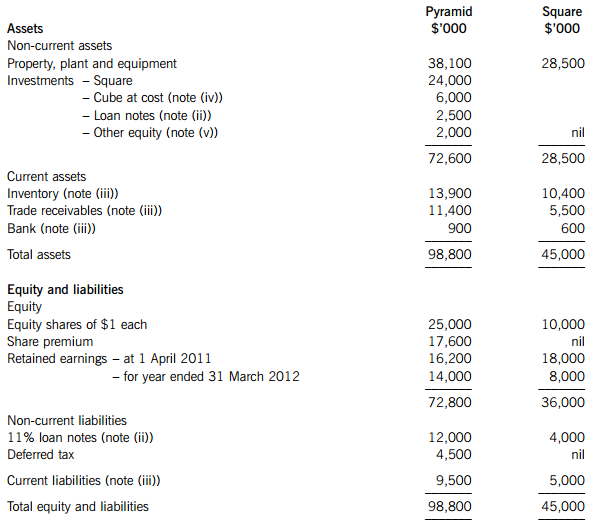

The summarised statements of financial position of the two companies as at 31 March 2012 are:

The following information is relevant:

(i) At the date of acquisition, Pyramid conducted a fair value exercise on Square’s net assets which were equal to their carrying amounts with the following exceptions:

– An item of plant had a fair value of $3 million above its carrying amount. At the date of acquisition it had a remaining life of five years. Ignore deferred tax relating to this fair value.

– Square had an unrecorded deferred tax liability of $1 million, which was unchanged as at 31 March 2012.

Pyramid’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose a share price for Square of $3·50 each is representative of the fair value of the shares held by the non-controlling interest.

(ii) Immediately after the acquisition, Square issued $4 million of 11% loan notes, $2·5 million of which were bought by Pyramid. All interest due on the loan notes as at 31 March 2012 has been paid and received.

(iii) Pyramid sells goods to Square at cost plus 50%. Below is a summary of the recorded activities for the year ended 31 March 2012 and balances as at 31 March 2012:

On 26 March 2012, Pyramid sold and despatched goods to Square, which Square did not record until they were received on 2 April 2012. Square’s inventory was counted on 31 March 2012 and does not include any goods purchased from Pyramid.

On 27 March 2012, Square remitted to Pyramid a cash payment which was not received by Pyramid until 4 April 2012. This payment accounted for the remaining difference on the current accounts.

(iv) Pyramid bought 1·5 million shares in Cube on 1 October 2011; this represents a holding of 30% of Cube’s equity. At 31 March 2012, Cube’s retained profits had increased by $2 million over their value at 1 October 2011. Pyramid uses equity accounting in its consolidated financial statements for its investment in Cube.

(v) The other equity investments of Pyramid are carried at their fair values on 1 April 2011. At 31 March 2012, these had increased to $2·8 million.

(vi) There were no impairment losses within the group during the year ended 31 March 2012.

Required:

Prepare the consolidated statement of financial position for Pyramid as at 31 March 2012.

第4题

Lily Window Glass Co (Lily) is a glass manufacturer, which operates from a large production facility, where it undertakes continuous production 24 hours a day, seven days a week. Also on this site are two warehouses, where the company’s raw materials and finished goods are stored. Lily’s year end is 31 December.

Lily is finalising the arrangements for the year-end inventory count, which is to be undertaken on 31 December 2012. The finished windows are stored within 20 aisles of the first warehouse. The second warehouse is for large piles of raw materials, such as sand, used in the manufacture of glass. The following arrangements have been made for the inventory count:

The warehouse manager will supervise the count as he is most familiar with the inventory. There will be ten teams of counters and each team will contain two members of staff, one from the finance and one from the manufacturing department. None of the warehouse staff, other than the manager, will be involved in the count.

Each team will count an aisle of finished goods by counting up and then down each aisle. As this process is systematic, it is not felt that the team will need to flag areas once counted. Once the team has finished counting an aisle, they will hand in their sheets and be given a set for another aisle of the warehouse. In addition to the above, to assist with the inventory counting, there will be two teams of counters from the internal audit department and they will perform. inventory counts.

The count sheets are sequentially numbered, and the product codes and descriptions are printed on them but no quantities. If the counters identify any inventory which is not on their sheets, then they are to enter the item on a separate sheet, which is not numbered. Once all counting is complete, the sequence of the sheets is checked and any additional sheets are also handed in at this stage. All sheets are completed in ink.

Any damaged goods identified by the counters will be too heavy to move to a central location, hence they are to be left where they are but the counter is to make a note on the inventory sheets detailing the level of damage.

As Lily undertakes continuous production, there will continue to be movements of raw materials and finished goods in and out of the warehouse during the count. These will be kept to a minimum where possible.

The level of work-in-progress in the manufacturing plant is to be assessed by the warehouse manager. It is likely that this will be an immaterial balance. In addition, the raw materials quantities are to be approximated by measuring the height and width of the raw material piles. In the past this task has been undertaken by a specialist; however, the warehouse manager feels confident that he can perform. this task.

Required:

(a) For the inventory count arrangements of Lily Window Glass Co:

(i) Identify and explain SIX deficiencies; and

(ii) Provide a recommendation to address each deficiency.

The total marks will be split equally between each part (12 marks)

You are the audit senior of Daffodil & Co and are responsible for the audit of inventory for Lily. You will be attending the year-end inventory count on 31 December 2012.

In addition, your manager wishes to utilise computer-assisted audit techniques for the first time for controls and substantive testing in auditing Lily Window Glass Co’s inventory.

Required:

(b) Describe the procedures to be undertaken by the auditor DURING the inventory count of Lily Window Glass Co in order to gain sufficient appropriate audit evidence. (6 marks)

(c) For the audit of the inventory cycle and year-end inventory balance of Lily Window Glass Co:

(i) Describe FOUR audit procedures that could be carried out using computer-assisted audit techniques (CAATS);

(ii) Explain the potential advantages of using CAATs; and

(iii) Explain the potential disadvantages of using CAATs.

The total marks will be split equally between each part (12 marks)

第5题

The following scenario relates to questions 1–5

You are an audit senior of Viola & Co and are currently conducting the audit of Poppy Co for the year ended 30 June 20X6.

Materiality has been set at $50,000, and you are carrying out the detailed substantive testing on the year-end payables balance. The audit manager has emphasised that understatement of the trade payables balance is a significant audit risk.

Below is an extract from the list of supplier statements as at 30 June 20X6 held by the company and corresponding payables ledger balances at the same date along with some commentary on the noted differences:

Carnation Co

The difference in the balance is due to an invoice which is under dispute due to faulty goods which were returned on 29 June 20X6.

Lily Co

The difference in the balance is due to the supplier statement showing an invoice dated 28 June 20X6 for $70,000 which was not recorded in the financial statements until after the year end. The payables clerk has advised the audit team that the invoice was not received until 2 July 20X6.

The audit manager has asked you to review the full list of trade payables and select balances on which supplier statement reconciliations will be performed.

Which of the following items should you select for testing?

(1) Suppliers with material balances at the year end

(2) Suppliers which have a high volume of business with Poppy Co

(3) Major suppliers with nil balances at the year end

(4) Major suppliers where the statement agrees to the ledger

A.1 only

B.1, 2 and 3 only

C.2 and 4 only

D.1, 2, 3 and 4

Which of the following audit procedures should be performed in relation to the balance with Lily Co to determine if the payables balance is understated?

A.Inspect the goods received note to determine when the goods were received

B.Inspect the purchase order to confirm it is dated before the year end

C.Review the post year-end cashbook for evidence of payment of the invoice

D.Send a confirmation request to Lily Co to confirm the outstanding balance

Which of the following audit procedures should be carried out to confirm the balance owing to Carnation Co?

(1) Review post year-end credit notes for evidence of acceptance of return

(2) Inspect pre year-end goods returned note in respect of the items sent back to the supplier

(3) Inspect post year-end cash book for evidence that the amount has been settled

A.1, 2 and 3

B.1 and 3 only

C.1 and 2 only

D.2 and 3 only

The audit manager has asked you to review the results of some statistical sampling testing, which resulted in 20% of the payables balance being tested.

The testing results indicate that there is a $45,000 error in the sample: $20,000 which is due to invoices not being recorded in the correct period as a result of weak controls and additionally there is a one-off error of $25,000 which was made by a temporary clerk.

What would be an appropriate course of action on the basis of these results?

A.The error is immaterial and therefore no further work is required

B.The effect of the control error should be projected across the whole population

C.Poppy Co should be asked to adjust the payables figure by $45,000

D.A different sample should be selected as these results are not reflective of the population

To help improve audit efficiency, Viola & Co is considering introducing the use of computer assisted audit techniques (CAATs) for some audits. You have been asked to consider how CAATs could be used during the audit of Poppy Co.

Which of the following is an example of using test data for trade payables testing?

A.Selecting a sample of supplier balances for testing using monetary unit sampling

B.Recalculating the ageing of trade payables to identify balances which may be in dispute

C.Calculation of trade payables days to use in analytical procedures

D.Inputting dummy purchase invoices into the client system to see if processed correctly

请帮忙给出每个问题的正确答案和分析,谢谢!

第6题

They () the conversation in a friendly atmosphere.

A.carried out

B.carried on

C.carried forward

D.carried with

第8题

A.Sam carried the watermelon on the bike

B.Lily carried the watermelon on the car

C.Watermelon is delicious

第9题

A.who

B.whom

C.which

D.whose

第10题

A.nines-dollars

B.nines-dollar

C.nine-dollars

D.nine-dollar

第11题

A.is carried out

B.is brought out

C.is fetched